Subscribe

SubscribeOn November 13, 2025, the Life Sciences Investment Forum brought together more than 180 leaders in the life sciences investment community for a day of dynamic conversations and strategic insights. Top decision-makers shared emerging trends and opportunities, how they’re navigating market headwinds, and what they expect for the industry in 2026 and beyond. Below are four takeaways from the discussions.

- Growth is the dominant narrative and the key valuation driver

Across biopharma, private equity (PE), and public markets, growth was repeatedly emphasized as the most important factor for valuation, fundraising, and multiple expansion.

- Large-cap pharma has driven most recent market value expansion, fueled by demand for large-population therapies (e.g., GLP-1s).

- Investors expect outsized returns for companies with predictable, rapid top-line growth.

- “Keep your eye on the top line” emerged as the #1 message to investors heading into 2026.

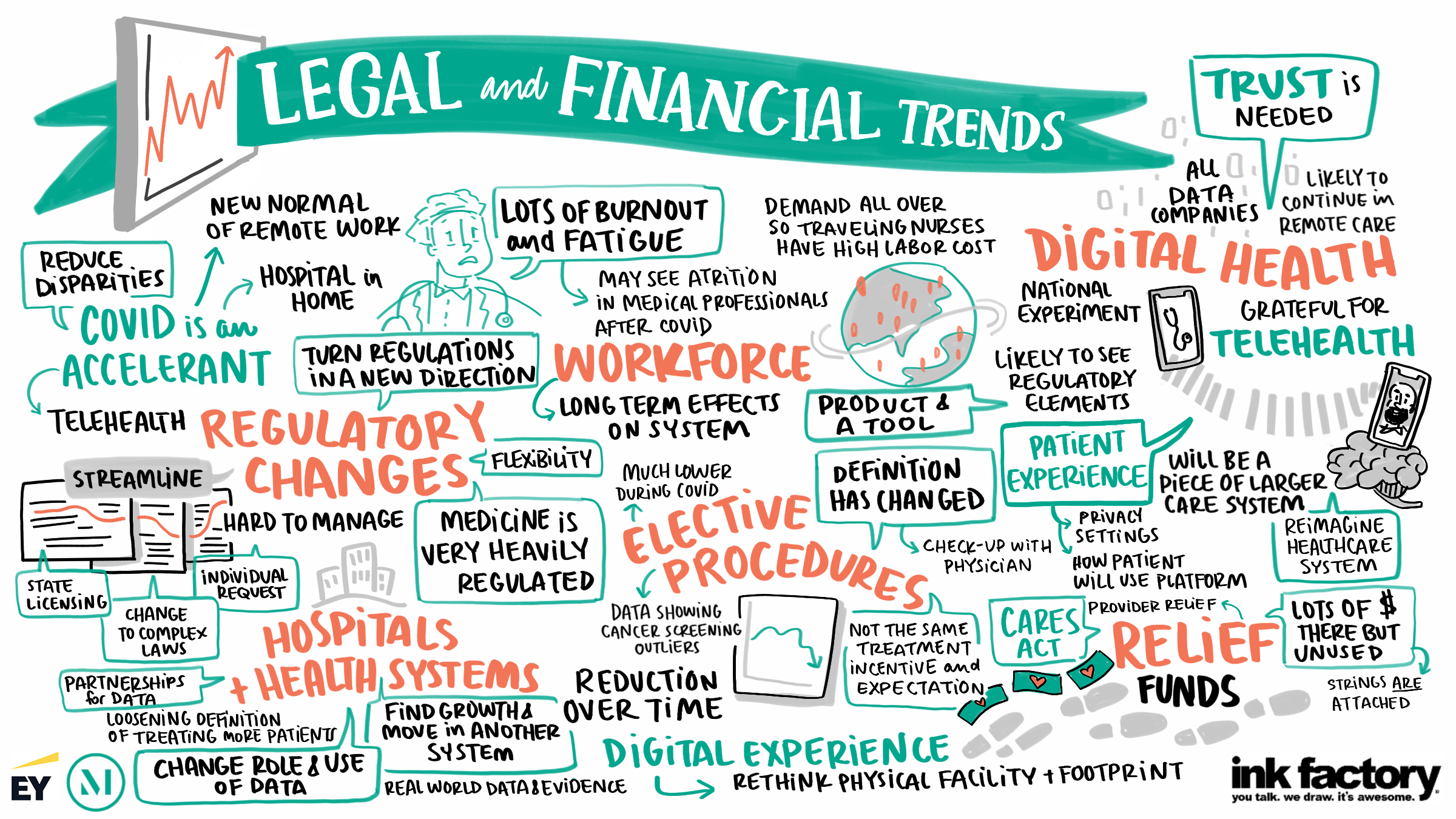

- Structural headwinds are mounting: Policy, pricing pressure, and healthcare costs

Regulation – not science – will be the primary gating factor in investment decisions over the next 12 to 24 months:

- Healthcare spending outpacing gross domestic product (GDP) is pushing pressure for cost controls.

- Most Favored Nation (MFN) pricing, drug price negotiations, and reimbursement shifts are creating real concern for biotech P&Ls, driving the need for tight forecasting and clean data.

- As transitions at the US Food and Drug Administration (FDA) are affecting predictability, companies must plan for worst-case regulatory scenarios and establish multiple backup plans.

- Early-stage is [...]

Continue Reading

read more